Key Takeaways

- US equities sold off sharply after a stronger-than-expected May payrolls report triggered a significant repricing of interest rate expectations, with markets now pricing potential Fed rate hikes rather than rate cuts.

- The payrolls surprise appears to have been driven largely by temporary factors, particularly a surge in leisure and hospitality hiring ahead of the FIFA World Cup, raising the possibility that labour market strength may prove transitory.

- While higher rates have created near-term volatility, the structural AI investment thesis remains intact, supported by strong earnings growth, continued corporate investment in AI infrastructure, and attractive growth-adjusted valuations across the AI value chain.

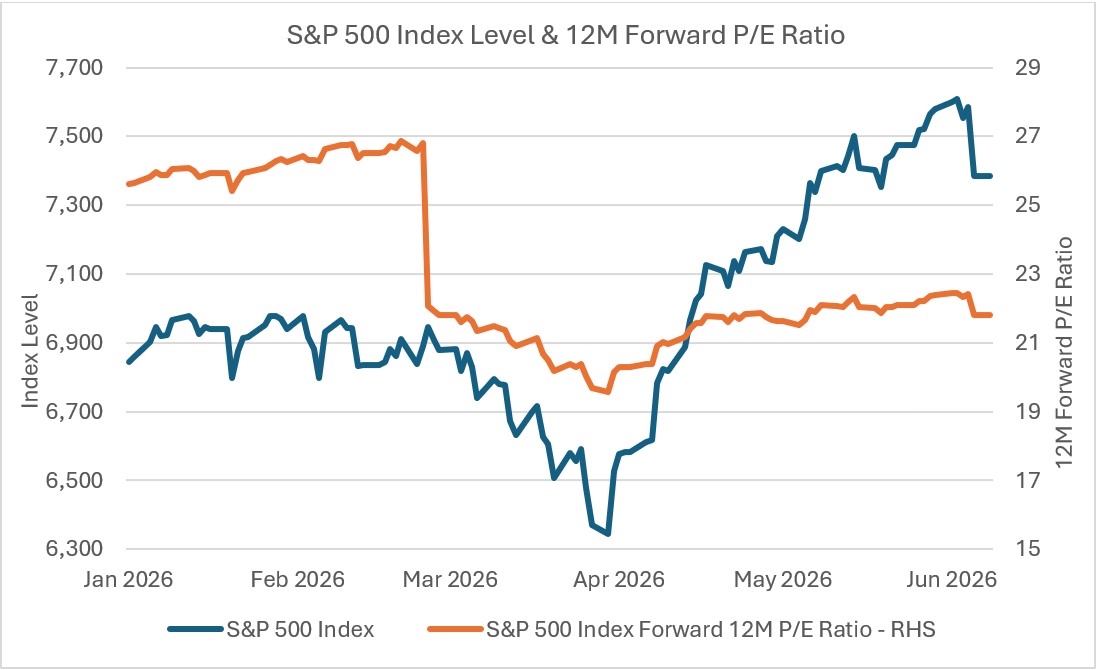

US equities sold off hard on Friday before staging a partial recovery on Monday, leaving the Nasdaq down 3.3% and the S&P 500 down 2.4% across both sessions as the rate repricing narrative dominated. Bonds offered little shelter with the 10-year yield pushing higher, and notably commodities provided no safe haven with Gold actually selling off, a divergence from a typical inflation scare where real assets would be expected to rally (refer to our previous Monday morning presentations on breakeven yields). The ASX opens this morning with two sessions of moves to absorb simultaneously.

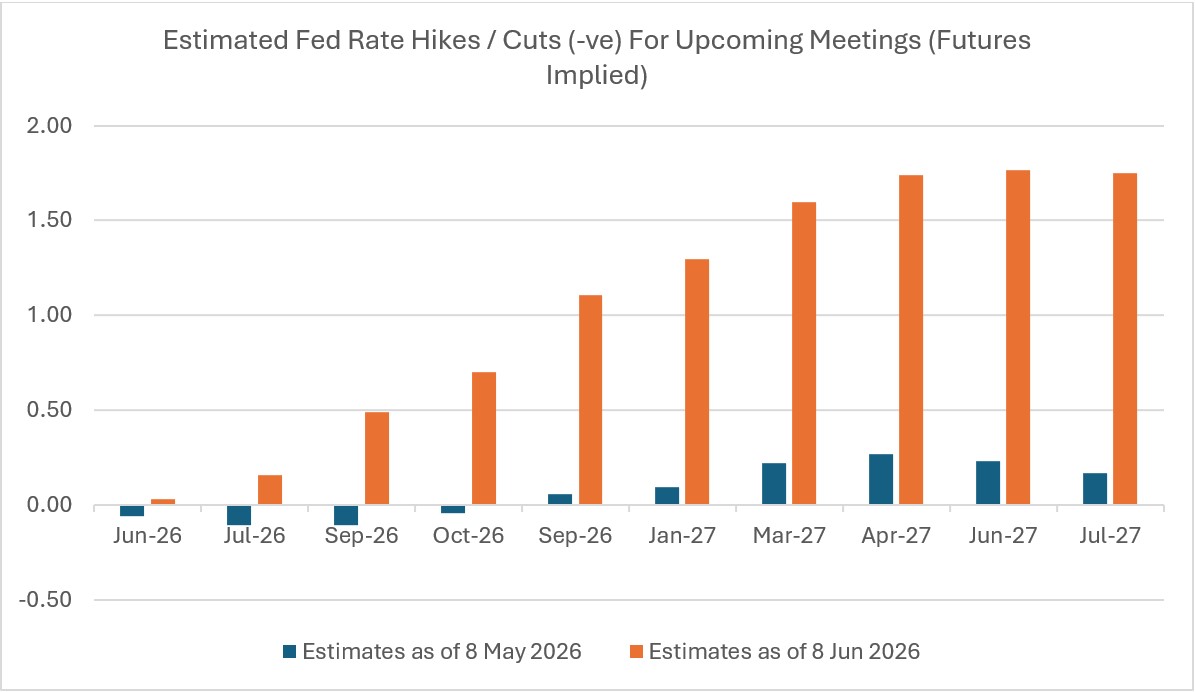

The trigger was May non-farm payrolls, which printed at 172,000 against a consensus of roughly 90,000. The beat was large enough to fully reprice the Fed's expected policy path. Cuts are no longer in the picture for 2026 and, for the first time this cycle, the market is now pricing approximately 1.5 to 2 rate hikes by mid-2027, with the first move most likely landing in Q4 2026.

Source: BLS, Bloomberg data as of 9 Jun 2026

How did NFP beat so much?

The headline number of 172,000 was more than double consensus, but the composition tells a different story. Leisure and hospitality added 70,000 jobs in May against a 12-month average of just 14,000, a fivefold surge that accounted for the entire beat over expectations on its own. Within that, food services and drinking places alone added 48,000. The timing is not coincidental as the FIFA World Cup kicks off this week across US host cities, and the data is entirely consistent with restaurants, bars, and hospitality venues pulling hiring forward ahead of the tournament. If that is the primary driver, May's strength is borrowed demand and June and July payrolls are likely to give a meaningful portion of it back.

A second factor worth watching is AI infrastructure buildout, where the ongoing wave of data centre and compute construction may be pulling forward hiring in facilities and support services in ways that are difficult to isolate in the headline figures. Both explanations share the same implication that the surge this month may be temporary, and we flag them as hypotheses given that if the next two prints confirm the trend the macro view has to adjust accordingly. But on current evidence, the Fed may be tightening into a one-month anomaly.

Why the market reacted so hard

The scale of Friday's selloff reflects positioning as much as the data itself, with hedge fund gross exposure heading into the print at the 99th percentile and put-to-call skew having essentially collapsed to zero, meaning the market was fully long with no hedges in place when the data landed. The week's prior headwinds compounded the vulnerability as Broadcom reported strong Q2 results but Q3 AI semiconductor guidance of US$16bn came in below expectations, sending the stock down around 15% and dragging the broader semiconductor sector lower. Alphabet's US$84.75bn equity raise, the largest in US market history, added to supply overhang concerns even though the deal itself priced well and traded above issue, and by the time Friday's payrolls number crossed the tape the market was already fragile enough that the reaction was always going to be outsized relative to the data's actual composition.

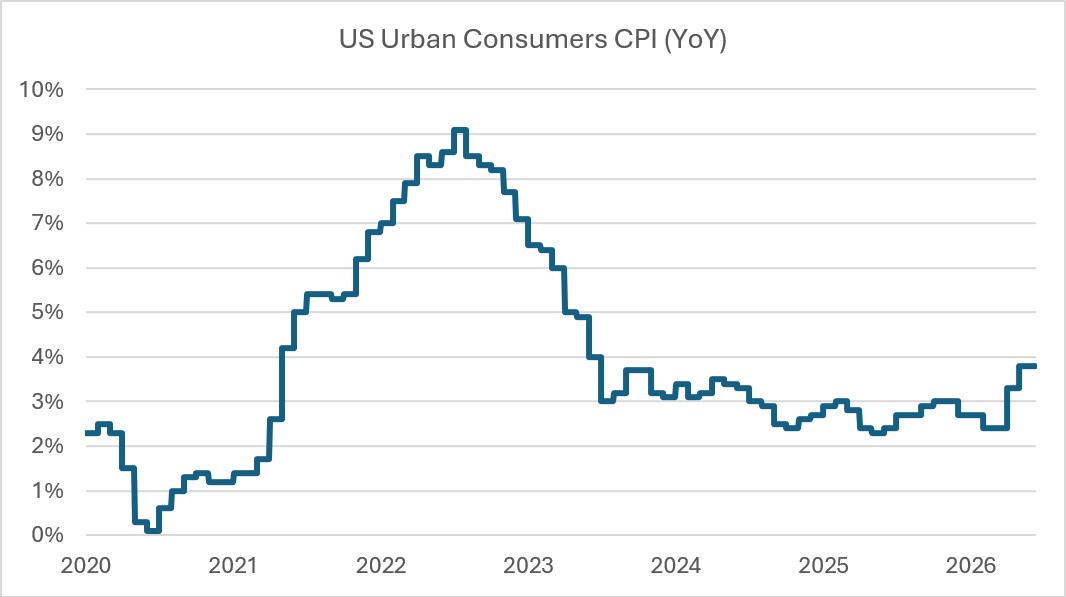

The next major catalyst is Wednesday's US CPI print, with the market currently pricing a 4.3% annual read, which would be the highest since April 2023. A firm number cements the hike thesis and keeps pressure on rates. A softer read gives the transitory argument room to develop and could stabilise sentiment ahead of the June 16-17 Fed meeting, which is now far more consequential than it looked a week ago.

Source: BLS, Bloomberg data as of 8 Jun 2026

Positioning: Hope for the best, prepare for the worst.

The structural case for the AI theme remains intact. Earnings across the value chain are strong as Broadcom's AI revenue doubled YoY even as the stock sold off on a guidance miss, and Alphabet's willingness to raise US$84.8bn to fund compute capacity reflects conviction rather than retreat. Corporate buybacks are running at roughly twice the recent historical pace. With US midterms approaching, the political incentive to avoid a sustained market dislocation is also real.

This is not a valuation-driven market in the way previous cycles were. The re-rating since 2023 has been largely earnings-driven, not multiple expansion, which makes the current environment structurally more resilient than the 2000 or 2021 precedent. Valuations have actually compressed on a forward basis as earnings growth has outpaced price appreciation. A rate-driven pullback is painful but it is a different kind of risk to a bubble deflating.

Source: Bloomberg data as of 8 Jun 2026

On a growth-adjusted basis, GXAI and U100 screen as genuinely cheap relative to both the Nasdaq 100 and MSCI World, with high quality businesses whose earnings trajectories compress valuations further without any multiple expansion assumption and superior risk-adjusted returns over the past year that directly address the volatility concern advisers will raise in the current environment.

Source: Bloomberg data as of 8 Jun 2026

The key is staying invested as the rally broadens and expressing that view through structures that do not leave you exposed to the single-name concentration risk that defined last week's volatility. GXAI and U100 give you full exposure to the AI growth story across the entire value chain, with capped weights ensuring that no single guidance miss can derail the position, which is precisely how you capture the next leg of the rally as it broadens beyond the Mag 7 with minimal binary downside that comes with owning the names directly.